The Thesis

The era of building on free frontier-grade weights is ending, and the companies that treated open-source AI as a permanent subsidy are about to discover it was a customer acquisition strategy.

The Signal

1. Meta ships Muse Spark as proprietary, abandoning Llama's open-weight model.

Meta Superintelligence Labs released Muse Spark on April 8, the first model from the unit Alexandr Wang has led since June 2025, and it is closed-source. Why it matters: Llama accumulated 1.2 billion downloads and offered startups an 88% cost reduction over proprietary APIs; that supply line is now frozen. The second-order effect: every company that embedded Llama as a foundation layer now faces a build-vs-buy reassessment on a timeline it did not choose, and the r/LocalLLaMA community is already treating this as a betrayal.

2. OpenAI enterprise revenue crosses 40% of total, on track for consumer parity.

OpenAI CRO Denise Dresser confirmed that enterprise now exceeds 40% of revenue, with paying business users at 9 million (up from 5 million in August) and Codex at 3 million weekly active users. Why it matters: enterprise is no longer the growth experiment; it is the business. The second-order effect: OpenAI's Frontier platform, which positions AI agents as a unified operating layer across enterprise systems, turns model capability into deployment infrastructure, and deployment infrastructure is where lock-in lives.

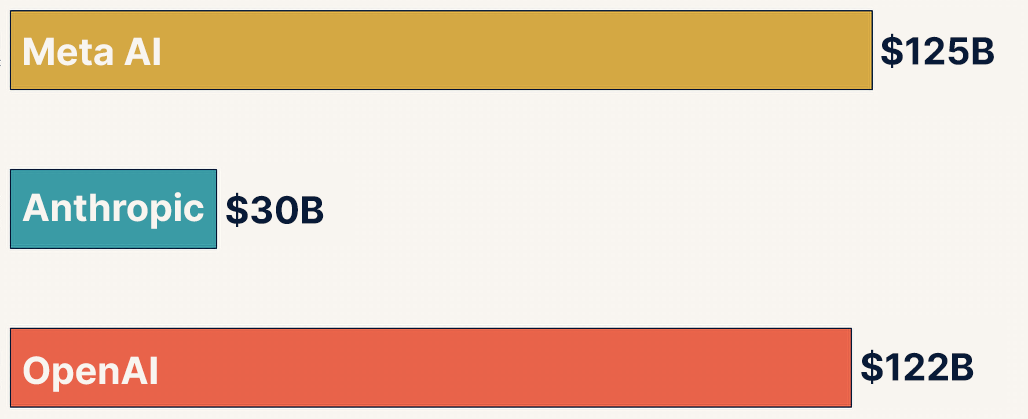

3. Capital concentration accelerates: $277 billion committed to three players in Q1.

OpenAI raised $122 billion at an $852 billion valuation. Anthropic's run rate hit $30 billion. Meta guided $115-135 billion in AI capex for 2026. Why it matters: the barrier to competing at the frontier is now measured in hundreds of billions, not tens. The second-order effect: mid-tier model providers face a squeeze between frontier labs with unlimited capital and open-source alternatives that still exist (Mistral, Qwen, GLM) but lack the distribution and ecosystem integration that Llama once offered.

The Playbook

Reassessing Your AI Foundation After the Open-Weight Freeze

If your product or infrastructure depends on Llama or any single open-weight model, run this audit this week:

- Map your Llama exposure. Identify every production system, fine-tuned model, and pipeline that uses Llama weights. Quantify the switching cost for each.

- Score your alternatives. Mistral, Qwen 3.6, and GLM-5 are viable open-weight replacements on benchmarks, but evaluate ecosystem maturity (tooling, community, enterprise support), not just performance.

- Price the proprietary fallback. Get current API pricing from Anthropic, OpenAI, and Google for your actual token volume. Compare total cost of ownership against self-hosting an alternative open model.

- Stress-test your vendor assumptions. If your vendor roadmap assumed Llama would remain free and open indefinitely, that was a subsidy, not a strategy. Identify which other vendor assumptions carry the same risk.

- Set a decision deadline. Do not wait for Meta to clarify its open-source timeline. Wang's "hope to open-source future versions" is a placeholder, not a commitment. Make your architecture decision on what is available today.

The Verification Test

The claim: Muse Spark is "competitive with GPT-5.4 and Claude Sonnet 4.6" across key tasks (Meta's published benchmarks).

The test: Independent benchmark reproduction by at least two external evaluators (e.g., LMSYS Chatbot Arena, Artificial Analysis) on the same task categories Meta highlighted.

What to watch for: Pass — Muse Spark places within 5% of GPT-5.4 and Claude Sonnet 4.6 on reasoning, coding, and multimodal tasks when tested by parties without a commercial relationship with Meta. Fail — Meta restricts API access to "select partners" long enough that independent testing is delayed past the news cycle, or benchmark categories are redefined after publication.

The Metric

$277 billion committed to three frontier AI players in Q1 2026 alone.

OpenAI ($122B raise), Anthropic ($30B run rate), and Meta ($125B capex midpoint) have collectively absorbed or committed more capital in one quarter than the entire global venture capital market deployed in 2024. This measures the concentration of AI infrastructure investment at the frontier. For operators, it means the platforms you build on are being shaped by capital allocation decisions of a scale that no startup or mid-market company can influence. Your leverage is in switching cost, not negotiation.

Sources: OpenAI, Anthropic, Meta 10-K guidance

The Lens

Horizon Search Institute

Human Performance: Cost per corporate learning hour jumped 34% in one year while total hours declined, signaling a shift from volume to intensity. ATD

Responsible AI: Anthropic's MCP crossed 97M installs; Linux Foundation taking it under open governance. Crescendo AI

Planetary Futures: Tufts neuro-symbolic AI system cuts inference energy consumption by 100x. Tufts University

Governance & Diplomacy: SCOTUS IEEPA tariff ruling forces shift to Section 122; 150-day clock expires July 24. Tax Foundation

Links Worth Your Time

- Enterprise Agentic AI Landscape 2026 — Vendor-by-vendor positioning map on trust vs. lock-in. The most useful single framework for enterprise AI procurement decisions published this quarter.

- Meta's Muse Spark: What Changed — Best independent analysis of the open-source-to-proprietary pivot and what it means for the developer ecosystem.

- OpenAI: The Next Phase of Enterprise AI — Dresser's framing of the "capability overhang" is worth reading for anyone trying to understand why enterprise AI adoption still lags model capability.

- Trump Tariffs After the Supreme Court — Clear overview of which tariffs survived the SCOTUS ruling, which are being refunded, and what the Section 122 replacement means for importers.

- Can Meta's Muse Spark Make Money? — The real question behind the model launch: whether Meta can convert 3 billion app users into a durable AI revenue stream.

Sources

- Axios — Meta debuts Muse Spark

- VentureBeat — Goodbye, Llama?

- RoboRhythms — Meta Launched Muse Spark

- OpenAI — The next phase of enterprise AI

- OpenAI — Introducing OpenAI Frontier

- OpenAI — $122 billion raise

- CNBC — Meta debuts new AI model

- CNBC — Can Muse Spark make money?

- Fortune — Meta unveils Muse Spark

- Crescendo AI — Latest AI News

- Tax Foundation — Tariff Tracker

- Kai Waehner — Enterprise Agentic AI Landscape 2026

- The Next Web — Muse Spark is closed source

- Kiplinger — Trump Tariffs After Supreme Court

The Searchlight is a weekly field memo. It is not investment advice. Views are the editor's own.